Opinion: This Is The Best Big Short For When The Silicon Valley Bubble Pops

There is close to $1 trillion worth of subprime paper valuations in U.S. private tech stocks. This is not going to end well.

Almost half the unicorns have fake and misleading valuations. Some companies valued at more than $1 billion have made such generous promises to their preferred shareholders that their common shares are nearly worthless, according to new research.

Private investors are sobering up to the fact that more than 90 percent of private tech valuations are fake and don’t rely on successful IPOs, cash, or profits but rely instead on fake valuations and finding a bigger fool to keep the Ponzi scheme going.

There’s a widening disconnect between bearish tech funding trends, weak IPO volume, bubblelicious valuations, misleading representations to investors, weak IPO performance and Nasdaq record highs. This disconnect tells the story of a set-up for very profitable trades for those who can recognize and exploit this market disconnect at the right time.

If there is a severe crash in private tech that feeds on itself, there is one stock that stands out that you probably want consider for short exposure or a hedge.

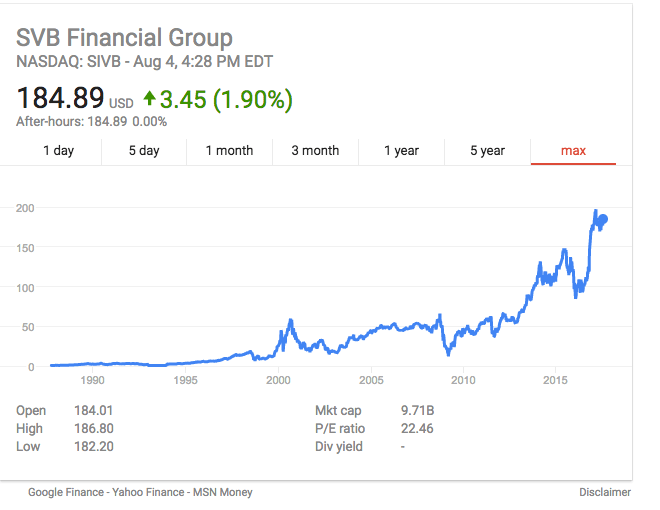

Silicon Valley Bank or SVB Financial Group (SIVB) is the hometown bank of private tech. It’s the banker of choice in Silicon Valley and as frothy unicorn valuations have risen, so has its stock.

Seed-stage financing for startups has slowed down 40 percent since the peak in mid-2015, Reuters reported last week. Although the Nasdaq has gained 21 percent year-to-date and 25 percent over the last 12 months, the Sharepost 100 Fund — a proxy for private tech — is down 4.6 percent YTD and down 2 percent over the last 12 months.

Because the IPO door is largely closed to private tech companies, they rely on more speculative funding rounds or hopes of getting acquired rather than conventional business protections of profits and cash flow.

Similar to the instruments in the subprime crisis, private tech has a lot of mark-to-mystery qualities where the accounting ranges from creative to outright fraudulent. The term is often used behind closed doors with this no-revenue formula. It’s a play on the common term for a more logical investment practice called mark-to-market, which is used to create a realistic appraisal of a company’s financial assets.

“VCs can create this mark-to-mystery valuation because as long as there are no numbers, I can have whatever mark I want for an external valuation of a startup,” said venture capitalist Paul Kedrosky.

Kedrosky explained the problems with the private tech sector this way:

“It serves the interest of the investors who can come up with whatever valuation they want when there are no revenues,” said Kedrosky, a venture investor and entrepreneur. “Once there is no revenue, there is no science, and it all just becomes finger-in-the-wind valuations.”

How much “fake valuation” paper is out there in private tech? What happens if the music stops and there are no IPOs, no big exits, no more venture debt, and no new funding for the paper underneath these companies?

The paper valuations underneath these mostly unprofitable companies could be more than $1 trillion. As so-called unicorns — those startups valued at $1 billion or more — are thought to be valued close to $700M in aggregate (U.S. only).

Almost half of unicorns have fake and misleading valuations, according to Will Gornall and Ilya Strebulaev, two professors at Stanford University and the University of British Columbia. These are some findings from their research:

We found that the average highly-valued venture capital-backed company reported a valuation 49 percent above its fair value. But, when the valuation was recalculated using the financial model developed by Ilya and I — which derives a fair valuation of each class of shares of VC-backed companies by taking into account the intricacies of contractual cash flow terms — almost half of these companies lost their unicorn status, with 11 percent being overvalued by more than 100 percent. Some unicorns have made such generous promises to their preferred shareholders that their common shares are nearly worthless.

This is happening because current valuations make a misleading assumption: that a company’s shares have the same price as the most recently issued shares. This oversimplification significantly inflates valuations, since the most recently-issued shares almost always include perks not found in previously-issued shares.

Specifically, we found that 53 percent of unicorns gave their most recent investors either a return guarantee in IPO (14 percent), the ability to block IPOs that did not return most of

their investment (20 percent), seniority over all other investors (31 percent), or other important terms.

The Silicon Valley Bank stock is up more than 78 percent in the last 12 months and 222 percent over the last five years. Here is how one prominent venture capitalist described the business model:

The bank, which recently opened an office in Santa Monica, is more willing than others to focus on a startup’s growth prospects rather than its current financial condition and to lend money so businesses can expand while awaiting the next round of venture capital funding, said investor Mark Suster, a client and managing partner at Upfront Ventures in Los Angeles.

When the music is loud at the bubble party and everyone is dancing, Silicon Valley Bank may be the stock to own. However, when the bubble music stops, it may be the best stock to short or use as a hedge.

The rapidly declining fundamentals in private tech don’t align with the current stock price.

A recent investment presentation of Silicon Valley Bank narrowly describes two fundamental growth drivers:

- Significant client funding and exit activity.

- Healthy Increases in early-stage and private equity client counts.

Essentially, the growth of the bank is dependent on more speculative investment in startups and more exits. On these matters, you don’t have to guess: Valuations, funding, and M&A activity are all slowing down in private tech. Acquisitions by large tech companies are on track for the fourth consecutive yearly slowdown, according to CB Insights.

This is not a situation where you have to guess what will happen in the future. The bank highlights “net warrant gains have exceeded early-stage loan losses over time.” The bank cites $88 million in aggregate warrant gains net of early stage losses between 2002 and YTD 2017. The “over time” part is cute, but how are those startup warrants doing now?

The bank’s net gains on warrants collapsed by 46 percent in 2015 to $38 million and then to another whopping 81 percent in 2016 to $7 million. The values are not as important as what the trends and implications are.

The bigger picture is the warrant portfolio was not able to match up with the net charge-off losses during the last financial crisis. Warrants less NCOs were $58 million in 2009 and are

pacing down about $48 million in 2017 but are likely to get worse, possibly busting through the prior record of minus $58 million.

I don’t really care about the relatively small numbers. The bank can easily absorb that with its balance sheet, but it tells me that things are rapidly going in the wrong direction in private tech and if this is the case, it will impact other parts of their business, such as client deposits.

Unprofitable businesses will bleed more cash as funding dries up.

Things are going in the wrong direction. All the fundamentals are screaming you are heading into a nasty bear market in private tech with close to $1 trillion of paper valuations backing unprofitable startups.

You would think Wall Street analysts would be focused on the facts on the ground but mostly they are bullish on the Silicon Valley Bank stock, just as they are in every bubble. David Long, an analyst at Raymond James, has a $224 target price on the Silicon Valley Bank stock and explains his bubblicious reasoning this way in a Barrons report:

“We believe there’s still more to come,” said Long, whose $224 price target is 25 percent above its $178 price. “Silicon Valley is strategically positioned to grow even more from events now unfolding, such as rate hikes, lower corporate tax rates, and improvements in the initial-public-offering market.”

Although the IPO market is better than last year (up 73 percent year-on-year), it is already underperforming expectations with the weak IPO performance of Snap and Blue Apron (a meal kit delivery business) likely leading to more investor caution.

On the downside, fundamentals are deteriorating in the private tech sector, in Silicon Valley Bank’s warrant portfolio, and in the startup loan portfolio. With so many of the Silicon Valley Bank bulls betting on rate hikes, corporate tax cuts, and a booming IPO market, how long can this speculation support the bubbly stock price? Investors betting against the bank probably need patience for the music to stop completely — likely a six-to-12-month time horizon.

As the great Anthony Scaramucci said, the “fish stinks from the head down.” A very trigger happy SoftBank reportedly backed away from investing in Uber on valuation, The Information recently reported. SoftBank wanted a price of $45 billion while Uber’s last round was $70 billion. If this transaction closed at the $45-billion valuation, this would have put the top unicorn into a 33-percent bear market decline.

Uber investor Benchmark Capital was smartly trying to cash out before all this implodes and couldn’t find foreign money to dump their shares. When more and more American investors can smell the stinky fish (fake valuations), the trend has been to go find some trigger-happy

foreign money, usually in the Middle East or Asia. In the 2007 mortgage subprime crisis, investors in Germany were the preferred fools to be found as the music started to turn down in volume. There are fewer and fewer fools to find here in the U.S. to write checks at current bubblelicious valuations.

If the price of Uber’s private stock gets cut by 50 percent, this has big implications for Silicon Valley Bank as the fish stinks from the head down.

Uber is not the only unicorn darling whose stock may slip into bear market territory. The online lender Prosper saw its valuation plummet 70 percent on its most recent funding round. Fidelity marked down Pinterest 17 percent last month.

You would see more down rounds in private tech but there is a nefarious game being played, where “dirty terms” are traded in exchange for a higher valuation to make it appear that the valuation trend is going in the right direction.

If the term sheets were clean and normal, the mark on the valuation would be lower, or a down round. As the market deteriorates, there are more and dirty terms hiding the fact that there is actually a bear market in the stock, or that the valuation has stopped increasing.

Venture capital legend Bill Gurley has repeatedly warned of a pending bubble bust and the increasing popularity of dirty terms:

Who are the Sharks? These are sophisticated and opportunistic investors that instinctively understand the aforementioned biases of the participants and know exactly how to craft investments that can exploit the situation, Gurley said. They lie in wait of these exact situations, and salivate at the opportunity to exercise their advantage.

“Dirty” or structured term sheets are proposed investments where the majority of the economic gains for the investor come not from the headline valuation, but rather through a series of dirty terms that are hidden deeper in the document. This allows the shark to meet the valuation “ask” of the entrepreneur and VC board member, all the while knowing that they will make excellent returns, even at exits that are far below the cover valuation.

Examples of dirty terms include guaranteed IPO returns, ratchets, PIK Dividends, series-based M&A vetoes, and superior preferences or liquidity rights. The typical Silicon Valley term sheet does not include such terms. The reason these terms can produce returns by themselves is that they set the stage for a rejiggering of the capitalization table at some point in the future. This is why the founder and their VC BOD member can still hold onto the illusion that everything is fine. The adjustment does not happen now, it will happen later.

Dirty term sheets are a massive problem for two reasons. One is that they “unpack” or “explode” at some point in the future. You can no longer simply look at the cap table and estimate your return. Once you have accepted a dirty offering, the payout at each potential future valuation requires a complex analysis, where the return for the shark is calculated first, and then the remains are shared by everyone else. The second reason they are a massive problem is that their complexity will render future financings all but impossible.

Any investor asked to follow a dirty offering will look at the complexity of the previous offering and likely opt out. This severely heightens the risk of either running out of money or

a complete recapitalization that wipes out previous shareholders (founder, employees, and investors alike). So, while it may seem innocuous to take such a round, and while it will solve your short term emotional biases and concerns, you may be putting your whole company in a much riskier position without even knowing it.Some later-stage investors may be tempted to become sharks themselves and start including structured terms into their own term sheets. Following through and succeeding at such a strategy will require these investors to truly embrace being a shark. They will need to be comfortable knowing that they are adverse to and in conflict with the founders, employees, and other investors on the capitalization chart. And they will need to be content knowing that they can win while others lose. This is not for the faint of heart, and certainly is not consistent with the typical investor behavior of the past several years.

Why you need to know about dirty terms

So why are the dirty terms important in evaluating the stock of Silicon Valley Bank? The $1 trillion of unprofitable and funny paper in private tech is rapidly becoming subprime, with dirty terms and valuations going the wrong way. The capital slushing around has to find a home so you are seeing more capital to go to weak ideas and weaker entrepreneurs. You have more and more celebrities becoming VCs and angel investors. It’s not to the point where the strawberry picker is buying a $400,000 house in California without documentation, but folks we have a massive problem brewing.

The IPO and M&A markets are not strong enough or dumb enough to pay for the dirty, misleading, and sometimes fraudulent valuations and the bubble music is about to stop. The bubble music is already being turned down in volume but this is not reflected in Silicon Valley Bank’s stock. Not yet.

Investors and traders would be wise to identify who has the most exposure to this increasingly dirty subprime sector before it completely falls apart.

Whether it’s the unprofitable Nasdaq tech stocks of 2000, subprime mortgages in 2008, or the $1 trillion in subprime private tech paper today, when the bigger fool can’t be found anymore, the market can turn fast and it turns into a vicious cycle that the experts say they could never have predicted.

Late in the game, some elite U.S. VC investors are now desperately trying to cash out with Asian or Middle East investors, who may end up being the johnny-come-lately German subprime buyers of the next tech crash.